Why You Don’t Need To Be Afraid of Today’s Mortgage Rates

Mortgage

Mortgage

Mortgage rates have been the monster under the bed for a while. Every time they tick up, people flinch and say, “Maybe I’ll wait.” But here’s the twist. Waiting for that perfect 5-point-something rate could end up haunting your wallet later.

According to the National Association of Realtors (NAR):

“. . . a 30-year fixed rate mortgage of 6% would make the median-priced home affordable for about 5.5 million more households—including 1.6 million renters. If rates were to hit that magic number, it’s likely that about 10%—or 550,000—of those additional households would buy a home over the next 12 or 18 months.”

When the market hits that mortgage rate sweet spot, as expert forecasters are starting to say is more likely in 2026, the psychological shift to lower rates will kick in for more of today’s hopeful buyers. That will unleash some pent-up demand that’s been waiting on the sidelines, and the increase in activity will cause prices to rise.

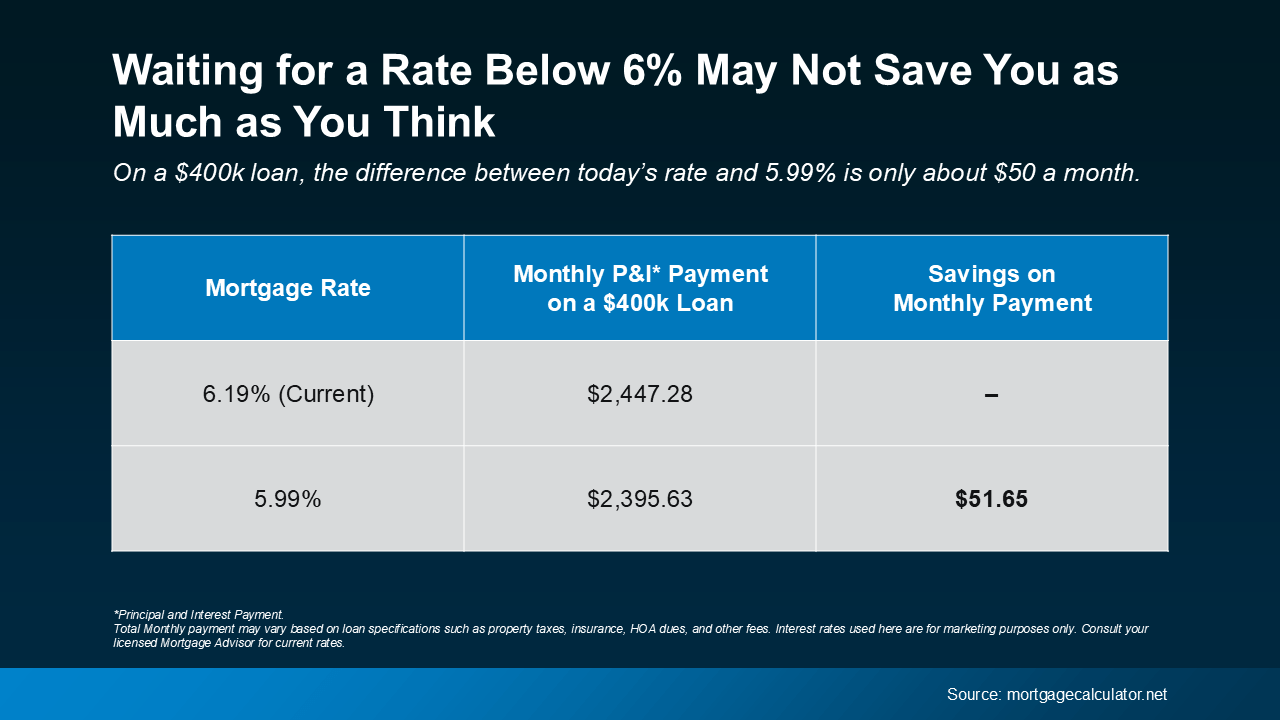

And while a 5.99% rate might sound like a big win, if you’re waiting for that number to make your move, it might not actually save you as much as you think. Here’s how the math looks when you run the numbers (see chart below):

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 a month. That’s less than many people spend on weekly coffee runs or occasional DoorDash orders. And as prices tick up with more buyers in the market, that could quickly negate any of your potential savings.

So, if you’re waiting for 5.99%, that difference might not be worth missing out on today’s opportunities, like having more homes to choose from, better negotiation leverage with today’s sellers, and fewer buyers out there looking for the same houses.

Because the reality is, those benefits start to slip away when more buyers begin to make their moves – and a rate under 6% is exactly they’re waiting for.

Jessica Lautz, Deputy Chief Economist and VP of Research at NAR, says:

“Over the last 5 weeks, mortgage rates have averaged 6.31%. This has provided savvy buyers a sweet spot to reexamine the home search process with more inventory, widening their choices.”

And like Matt Vernon, Head of Retail Lending at Bank of America, notes:

“Rather than waiting it out for a rate that they like better, hopeful homebuyers should assess their personal financial situation—if the house is right for them, and the upfront and monthly payments are affordable, it could be the right chance to make a move.”

If moving at today’s rate scares you, remember, waiting doesn’t always pay off. Once rates dip below 6%, as some experts project they’ll do next year, more buyers (and higher prices) will be back.

So, don’t be afraid of today’s mortgage rates. Because if you’re ready, this might just be your chance to make your move before the market wakes up again.

Stay up to date on the latest real estate trends.

Mortgage

The bigger opportunity is the Spring season as a whole

New Listing

2 beds | 1.5 baths | 1,279 sq ft

Mortgage

Work with a trusted lender and take steps that’ll help you get the best rate possible

Mortgage

The right home improvements today can set you up for success tomorrow

Mortgage

The pressure buyers felt over the last few years is finally starting to ease

Mortgage

Buying your first home doesn’t mean you have to have everything figured out

Mortgage

One of the biggest dealbreakers for buyers today is inspection issues

New Listing

2 beds | 1 bath | 689 sq ft

Mortgage

Homeowners today have far more equity and flexibility than they did during the crash.

You’ve got questions and we can’t wait to answer them.